Every underwriting decision is, at its core, a classification problem. Should this risk be bound or declined? Is this submission likely to generate profitable loss experience, or will it erode margins? Will this policyholder renew, or are they likely to lapse? Binary classification models are one of the foundational techniques in machine learning, and they give underwriters a structured, data-driven answer to each of these questions before a policy is ever issued.

How Binary Classification Works in Insurance

A binary classification model is a supervised machine learning algorithm trained to assign any input, like a submission, a claim, or a renewal, to one of two mutually exclusive outcomes. In insurance, those outcomes map directly to the decisions underwriters make every day: bound or declined, fraudulent or legitimate, likely to renew or likely to lapse.

The model learns by training on historical data, which includes thousands or millions of past policies paired with their actual outcomes. It identifies which input variables, like loss history, coverage type, industry classification, geography, or third-party enrichment signals, most reliably predict which outcome a new submission will produce. Once trained, the model scores every incoming submission against those learned patterns and returns a probability. Submissions above a defined threshold route one way, and those below route another.

Common algorithms used in insurance binary classification include logistic regression, gradient boosting, random forests, and neural networks. The Casualty Actuarial Society’s (CAS) research on underwriting applications of predictive analytics identifies gradient boosting and random forests as particularly well-suited to insurance risk classification because of their ability to capture non-linear relationships and complex variable interactions that traditional generalized linear models cannot accommodate. (Source) The CAS specifically documents insurers building supervised models on historical exposure data to optimize selection on loss ratio or combined ratio. This is a direct application of binary classification logic.

Application 1: Appetite Matching and Submission Triage

Before an underwriter reads a single line of a submission, a binary classifier has already made a consequential decision: does this risk fall within appetite, or does it not? That determination is where classification models deliver their most immediate operational value in underwriting.

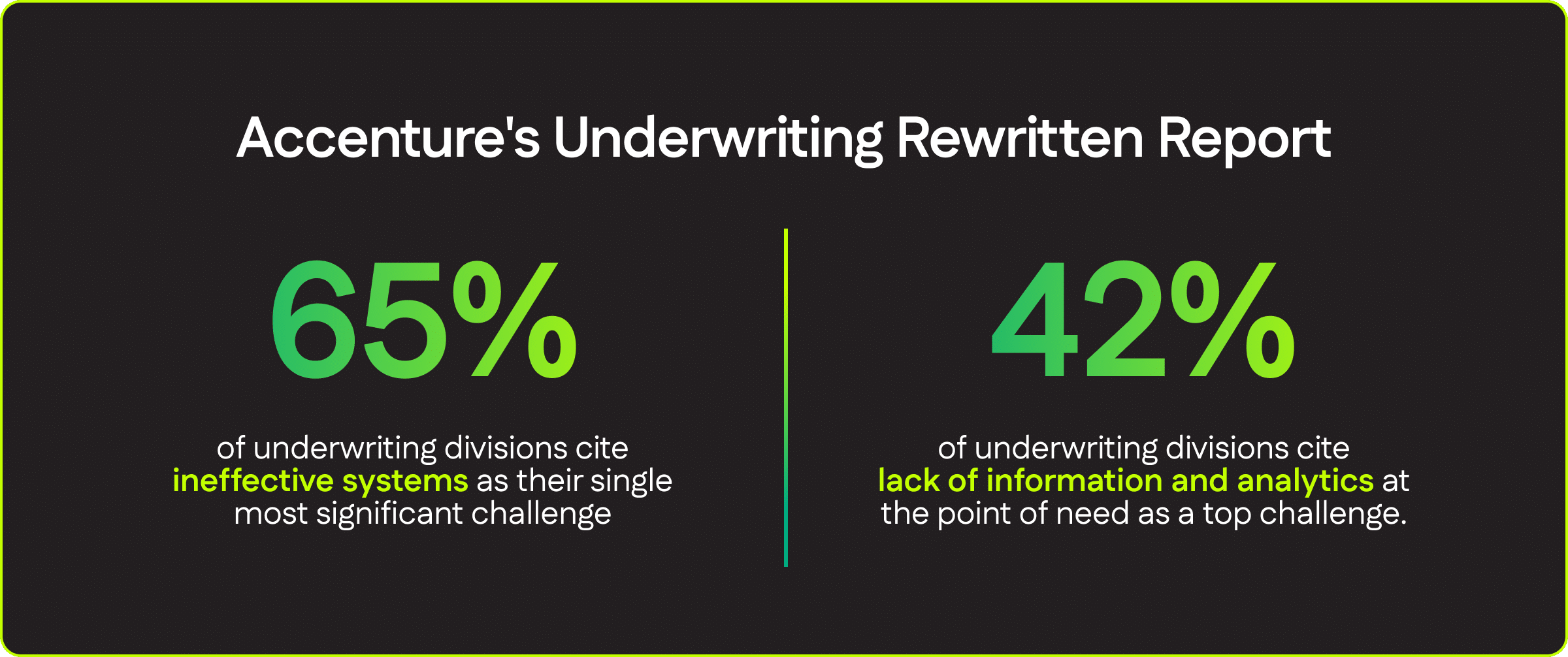

Additionally, Accenture’s Underwriting Rewritten report identifies ineffective systems as the single most cited challenge by underwriting divisions (65%), with lack of information and analytics at the point of need following closely behind (42%). (Source) Binary classification at the triage stage directly resolves both problems by replacing manual appetite-checking with automated scoring and surfaces the data an underwriter needs at the exact moment a referral decision is made.

Application 2: Application-Stage Fraud Scoring

The most cost-effective point to stop fraudulent exposure is before a policy is bound. According to the Insurance Information Institute, citing Coalition Against Insurance Fraud data, insurance fraud costs the U.S. $308.6 billion annually across all lines. (Source) Additionally, property-casualty fraud accounts for approximately 10% of all P&C losses and loss adjustment expenses. (Source)

Classification models trained on historical fraud outcomes learn which submission-level signals are disproportionately associated with fraudulent policies. The model scores each incoming application against those learned patterns and returns a probability, routing high-scoring submissions for enhanced review before binding. McKinsey’s analysis identifies traditional predictive analytics for fraud detection as the most established application of AI across the insurance value chain, the use case where supervised machine learning is already operating at production scale across the largest carriers. (Source)

Application 3: Non-Renewal Prediction at the Portfolio Level

Binary classification does not only apply at the front of the policy lifecycle. At renewal, a classifier trained on historical retention and lapse outcomes enables carriers to identify which policyholders are statistically likely to non-renew before the renewal cycle begins, shifting retention from a reactive scramble into a structured underwriting discipline.

Peer-reviewed research examined renewal classification across a real-world portfolio of more than 70,000 motor policies and found that binary classifiers achieved predictive accuracy above 98% in identifying which policyholders would lapse. (Source) The study demonstrates that renewal likelihood, treated as a binary classification problem, is highly predictable from a tractable set of policy-level variables, and that the model’s signals map cleanly onto the commercial levers available to underwriting and retention teams.

Key Takeaways on Binary Classification in Insurance

Applied consistently across all three domains — submission triage, fraud scoring, and renewal prediction — binary classification transforms underwriting from a series of isolated decisions into a continuous risk management function. Each individual classification is a small improvement in precision. The compounding effect across a large, active book is a structurally sounder carrier.

Pinpoint delivers the AI-powered infrastructure that allows carriers to operationalize precision risk scoring across selection, fraud detection, and renewal. Click here to learn more.