Traditionally, credit scoring models have been the bedrock of determining a potential insured’s risk level. However, these scores, which have only been around in their modern form since 1989, have started to fall by the wayside in the risk assessment process. Over time, it’s become clear that a historical snapshot of someone’s credit history isn’t as beneficial an indicator as their real-time data. Today, a new science of underwriting is emerging, leveraging high-velocity alternative data and advanced machine learning to refine insurability decisions. In this post, we explore how modern underwriting models are moving beyond static credit scores toward real-time data, explainable AI, and human-validated decisioning and why that shift matters for fairness, regulation, and risk accuracy.

The Shift to Real-Time Variables

Traditional scoring systems primarily focus on past behavior. In contrast, modern underwriting incorporates cash-flow data, utility payments, and transaction-level insights, among other metrics. Research indicates that variables such as income consistency and liquidity levels provide a more accurate, real-time snapshot of risk profile than a static FICO or CBIS score.

According to a 2024 study by the Poverty Action Lab, machine learning models utilizing digital transaction footprints can predict loss events more effectively than models relying solely on credit bureau data. This is particularly true for “credit invisible” populations. These are people who lack a traditional credit profile or profit tracking at the three major national credit bureaus. They are a significant portion of the population, estimated by PERC research to be 35 to 54 million Americans.

Fairness, Transparency, and Regulation in Insurance Underwriting

As carriers move toward more complex and accurate algorithms, the industry faces a critical juncture regarding regulatory readiness. Regulatory bodies, including the Financial Industry Regulatory Authority (FINRA) and the European Commission (via the EU AI Act), are shifting focus from “what” a model predicts to “how” it arrives at that conclusion.

Key regulatory expectations for 2026 include:

- Human-in-the-Loop (HITL): Explicit checkpoints where human judgment validates algorithmic outputs, particularly for denied applications.

- Algorithmic Auditing: Regular assessments to prevent “proxy discrimination,” where non-protected variables (like zip codes or educational background) unintentionally correlate with protected characteristics like race or gender.

- Data Lineage: Maintaining a clear audit trail of where data originated and how it was transformed before entering the model.

The Technical Frontier: Model Validation and XAI

The “Black Box” problem outlined above remains the primary hurdle for large-scale AI adoption in finance. To combat this, Explainable AI (XAI) has moved from a theoretical concept to a required component of model validation.

(XAI) Techniques

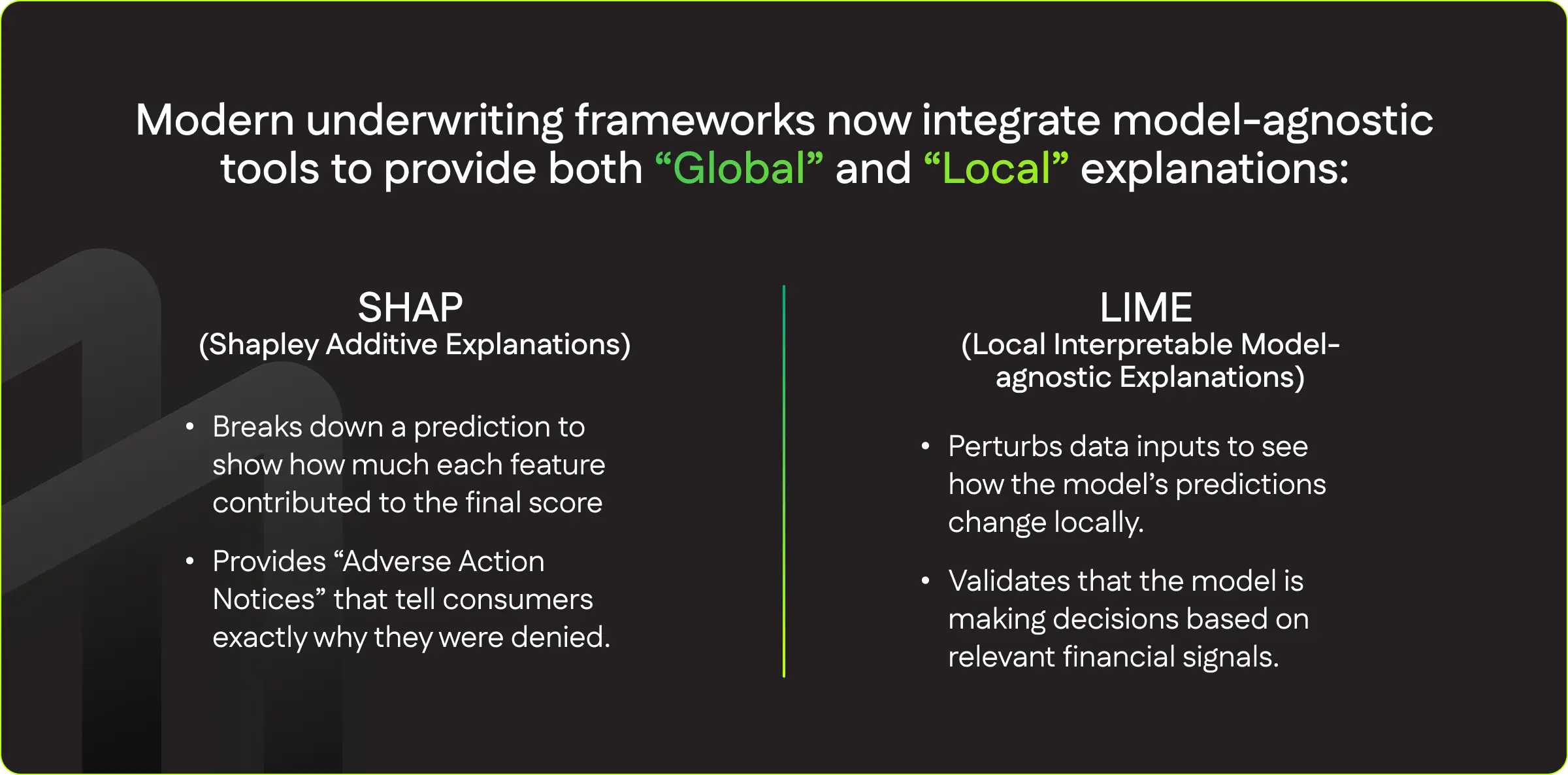

Modern underwriting frameworks now integrate model-agnostic tools to provide both “Global” and “Local” explanations:

- SHAP (Shapley Additive Explanations)

-

-

- Breaks down a prediction to show how much each feature contributed to the final score

- Provides “Adverse Action Notices” that tell consumers exactly why they were denied.

-

- LIME (Local Interpretable Model-agnostic Explanations)

-

- Perturbs data inputs to see how the model’s predictions change locally.

- Validates that the model is making decisions based on relevant financial signals.

Ensuring fairness is no longer just about removing sensitive attributes. Data ethics in 2026 focuses on Fairness-Aware Machine Learning, which utilizes specific metrics to detect bias:

- Demographic Parity: Ensures equal approval rates across different demographic groups.

- Equal Opportunity: Measures whether qualified applicants from different groups have the same probability of being approved.

Moving Forward

The transition to data-driven underwriting offers a dual promise: increased precision for carriers and expanded access for policyholders. However, the integrity of this “new science” depends on the industry’s ability to balance predictive power with ethical accountability.

Modern Underwriting Models: Signal Detection, Customization, and Fairness

Pinpoint Predictive models are at the forefront of modern underwriting, leveraging actual industry insurance loss and default data to identify nuanced risk signals that traditional credit scores often miss. Unlike legacy credit score approaches that rely on static historical information, Pinpoint’s models incorporate dynamic, feature-rich datasets to target real-world claims and default experiences, enabling more precise and relevant risk assessments.

These models are built custom for each loan type, insurer, lender, or line of business, allowing for the inclusion of variables tailored to specific risk profiles. During development, a broad set of candidate variables, ranging from marketing signals to transaction-level data, is rigorously evaluated for predictive power. Crucially, every variable considered for inclusion undergoes thorough testing to ensure it does not introduce discrimination based on race or social class.

This fairness assurance is achieved through several mechanisms:

- Proxy Discrimination Audits: Variables are statistically tested to ensure they do not serve as proxies for protected characteristics, such as race or socioeconomic status. For example, geographic or educational data are scrutinized to prevent indirect bias.

- Adverse Impact Metrics and Variance Testing by Protected Class: The models are evaluated using adverse impact metrics and variance testing, which analyze outcomes across protected classes to ensure that approval rates and predictive accuracy do not disproportionately disadvantage any group.

After deployment, Pinpoint Predictive models are subject to ongoing algorithmic auditing and human-in-the-loop validation, maintaining fairness and effectiveness as new data and regulatory standards emerge. This approach ensures that predictive power is balanced with ethical accountability, supporting both precision for lenders and insurance companies while expanding access for borrowers and insureds.

If you want to find out how Pinpoint can help improve your loss ratios and optimize your processes, book a discovery call to learn more.